By Robert Majdak Sr. MBA

Management Insights Group, LLC

July 5, 2026

EBITDA—earnings before interest, taxes, depreciation, and amortization—is the single most cited financial metric in for-profit valuation, lending, and management discourse, yet it is also among the most casually misapplied. A working command of what the number captures, how it is constructed, and where its limitations lie is not optional for anyone advising on transactions, credit facilities, or internal performance benchmarking.

What EBITDA Measures

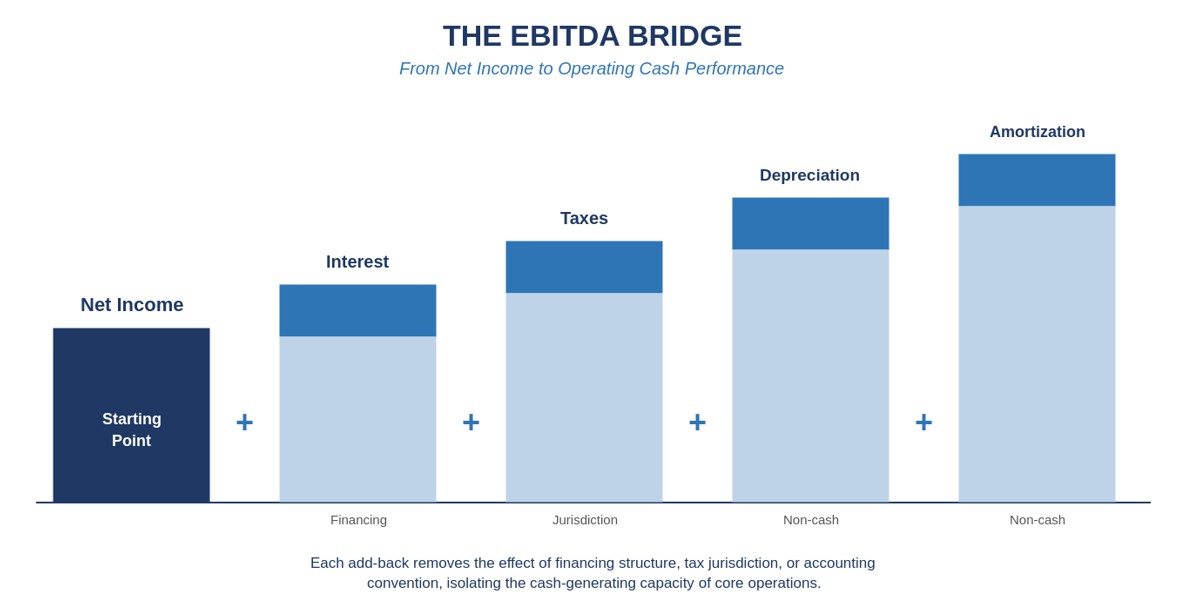

EBITDA begins with net income and adds back four categories of expense: interest, income taxes, depreciation, and amortization. Interest and taxes are added back because they reflect financing structure and jurisdiction rather than operating performance—two identical businesses can post radically different net income figures purely because one carries debt and the other does not, or because one operates in a low-tax state and the other does not. Depreciation and amortization are added back because they are non-cash charges that spread the cost of long-lived assets or intangibles over time according to accounting convention rather than actual cash outflow in the current period. Strip all four away, and what remains approximates the cash-generating capacity of the business’s core operations, independent of how it is financed, taxed, or how its balance sheet accounts for prior capital investment.

Figure 1: The EBITDA bridge from net income to operating cash performance.

Why the For-Profit Market Built Around It

Three forces explain EBITDA’s dominance in for-profit finance. The first is valuation. Buyers and sellers in private transactions routinely negotiate price as a multiple of trailing twelve-month or forward-projected EBITDA, because the multiple approach allows comparison across target companies that carry different debt loads, tax situations, and depreciation schedules. A business valued at six times EBITDA can be compared meaningfully against a competitor valued at seven times EBITDA in a way that a comparison of net income multiples cannot support, given how leverage and tax structure distort net income independent of operating quality.

The second force is credit. Commercial lenders and private credit funds build loan covenants directly around EBITDA, most commonly through a leverage ratio—total debt divided by EBITDA—and a coverage ratio—EBITDA divided by required debt service. These covenants function as early warning systems for lenders, and a borrower’s ability to stay within them frequently determines whether it retains access to a credit facility or triggers a default provision that accelerates repayment.

The third force is internal management discipline. Multi-unit or multi-subsidiary organizations use EBITDA to compare operating performance across units that may carry different capital structures, different depreciation schedules for equipment of different vintages, or different tax treatments across state lines. Removing those variables produces a cleaner read on which units are actually generating strong operating results and which are underperforming for reasons unrelated to financing choices made at the corporate level.

Where the Metric Breaks Down

EBITDA’s limitations deserve equal emphasis, because the metric is frequently presented to buyers and lenders as if it were a proxy for free cash flow, and it is not. EBITDA excludes capital expenditure entirely, which means a capital-intensive business—manufacturing, transportation, healthcare facilities—can show strong EBITDA while consuming substantial cash to maintain or replace its asset base. It also excludes changes in working capital, so a business growing receivables faster than it collects cash can show healthy EBITDA while quietly starving for liquidity. Analysts who stop at EBITDA without adjusting for maintenance capital expenditure and working capital movement are working from an incomplete picture, and sophisticated buyers and lenders always push past the headline number to unlevered free cash flow before finalizing terms.

A further caution applies to “adjusted EBITDA,” a variant frequently presented in seller-prepared financials that adds back one-time expenses, owner compensation normalization, and other discretionary items beyond the standard four. Every add-back in an adjusted EBITDA calculation deserves scrutiny, because sellers have every incentive to inflate the figure ahead of a sale process, and the gap between reported EBITDA and adjusted EBITDA is often where the real negotiation happens.

Applying the Discipline

For business owners preparing for a sale, a refinancing, or an internal performance review, the practical takeaway is straightforward: know your EBITDA calculation cold, understand every adjustment embedded in it, and be prepared to defend those adjustments with documentation. Buyers, lenders, and auditors will test the number, and a founder who cannot walk through the bridge from net income to EBITDA line by line loses credibility at exactly the moment credibility matters most.

-MIG

© Management Insights Group, LLC

Dallas/Fort Worth Texas Office