By Robert Majdak Sr. MBA

Management Insights Group, LLC

July 14, 2026

Why the Bottom Line Looks Different Without Owners

Net income is the most widely recognized measure of financial performance in the for-profit world, yet the term itself does not appear on a nonprofit’s audited financial statements. Board members and executives arriving from for-profit backgrounds frequently ask where net income sits on a nonprofit balance sheet, and the honest answer is that it does not exist in that form. Understanding why requires a clear look at what net income actually represents and how the nonprofit accounting framework restates the same underlying question in terms appropriate to an organization with no owners.

What Net Income Measures in the For-Profit Context

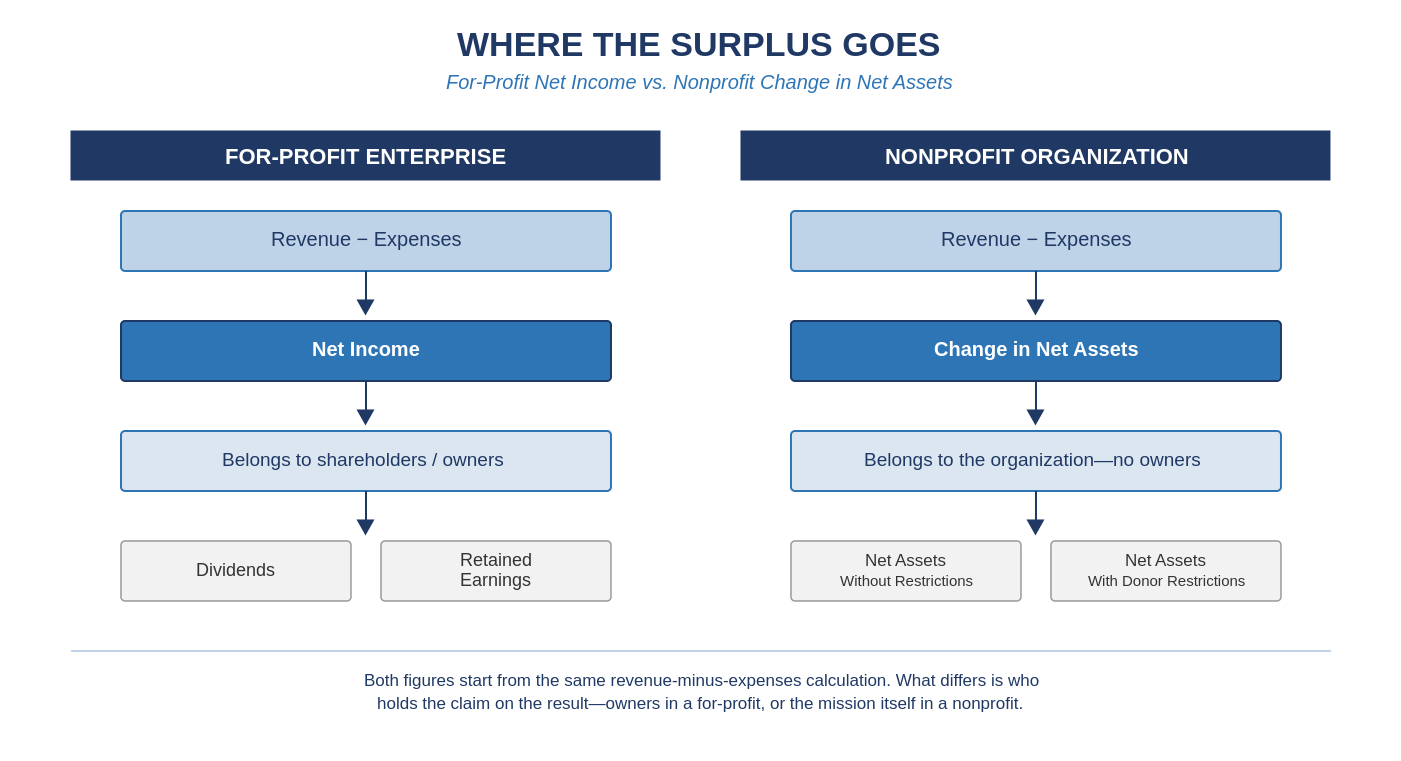

Net income is the residual left after subtracting all expenses, including cost of goods sold, operating expenses, interest, and taxes, from total revenue for a reporting period. It represents the return generated for the business’s owners—shareholders in a corporation, members in an LLC, partners in a partnership—and it is the figure from which dividends are declared, retained earnings accumulate, and equity value is ultimately built. Every dollar of net income belongs, in principle, to someone with an ownership claim on the enterprise. That ownership relationship is the organizing principle behind the entire for-profit accounting framework, and it is precisely the relationship that does not exist inside a nonprofit corporation.

The Nonprofit Equivalent: Change in Net Assets

Nonprofit organizations report a figure called the change in net assets, which appears on the Statement of Activities in place of net income on an income statement. The calculation is structurally similar—total revenue and support less total expenses—but the number that results belongs to no one. A 501(c)(3) organization has no shareholders, and any surplus generated in a given period cannot be distributed to individuals; it must be retained by the organization and applied toward its exempt purpose. This single distinction, the absence of a private ownership claim, is what separates a nonprofit’s change in net assets from a for-profit’s net income, even though both figures are calculated using the same basic revenue-minus-expenses logic.

Figure 1: Both calculations start the same way; the destination of the surplus is what differs.

Net Asset Classifications Matter More Than the Total

Where for-profit net income flows into a single retained earnings account, nonprofit net assets are classified according to donor-imposed restrictions, and this classification carries real operational consequences. Net assets without donor restrictions represent resources the organization can deploy at its own discretion, functioning as the closest proxy to for-profit retained earnings. Net assets with donor restrictions represent funds a donor has earmarked for a specific purpose, time period, or program, and the organization cannot redirect those funds regardless of how positive the overall change in net assets appears. A nonprofit can report a healthy positive change in net assets for the year while its unrestricted operating funds are dangerously thin, because the surplus sits almost entirely in restricted categories the organization cannot touch for payroll or overhead. Any board member evaluating nonprofit financial health has to look past the headline number and examine the composition of net assets by restriction category before drawing conclusions.

Why a Positive Number Is Not a Profit Motive

A recurring source of confusion is the assumption that a nonprofit posting a positive change in net assets is somehow behaving like a for-profit company chasing earnings. That assumption misreads the purpose of the metric entirely. A nonprofit needs periodic surpluses to build operating reserves, fund capital replacement, and absorb the inevitable variability in grant timing and donor giving. An organization that consistently breaks even or runs deficits has no cushion against a delayed grant payment or an unexpected facility repair, and its long-term sustainability suffers as a result. Regulators, watchdog organizations, and sophisticated funders understand this distinction well; a modest, consistent surplus is generally viewed as a sign of prudent management rather than mission drift, provided the organization can demonstrate that its program spending ratio remains appropriate to its exempt purpose.

Applying the Distinction in Practice

For executives and board members managing across both sectors, the practical discipline is to stop looking for net income on a nonprofit financial statement and instead evaluate the change in net assets alongside its restriction breakdown, the trend across several years, and the organization’s operating reserve target relative to its expense base. A single year’s change in net assets tells you almost nothing in isolation. The multi-year trend, read against liquidity and restriction composition, tells you whether the organization is building the financial resilience its mission requires.

-MIG

© Management Insights Group, LLC

Dallas/Fort Worth Texas Office